The UK's real partnership offer

On how the structure of the UK economy shapes what partners want from it

Next week the UK’s FCDO is co-hosting the Global Partnerships Conference in London, alongside South Africa, the Children’s Investment Fund Foundation and British International Investment.

It’s a difficult conference to host. The UK has cut back its aid spending faster than any G7 country. The conference can make the right noises about the UK’s commitment to shared challenges, but it is hard to avoid being defensive. It will not alter the arithmetic FCDO officials are working through as they look for cuts to make across programmes providing basic health and education services, or humanitarian assistance.

At the same time, there is a clear desire to look forward. It is being talked about as a conference on the future of ‘international development’ but not about ‘aid’. Much will be said about the UK’s stated ambition to think like an ‘investor’ rather than a ‘donor’.

It is worth stating up-front that catalytic finance and blended instruments will not directly replace programmes providing maternal health treatments. Not all flows of international money play the same role. At the same time, efforts to look at how the UK can usefully contribute to development beyond its aid budget should not be summarily dismissed. The UK’s international footprint does not stop neatly at the 0.3% or 0.5% of gross national income accounted as official development assistance. There is another 99% plus of economic activity that may also contribute to the stated goal to ‘drive shared growth and prosperity’.

Recognising the broader footprint is a useful starting point, but it does not automatically translate into a coherent strategy. What I want to suggest here is that the nature of the UK economy may not lend itself to unleashing major investment flows. The UK’s main attraction to partners and contributions to future economic development might be in areas that the conference does not really talk about much at all.

The UK’s economic structure shapes what kind of partnerships are possible

There is an instructive comparison to be made here with China and the Gulf (especially UAE). Over the past two decades, both have been major outward investors in emerging markets, and in neither case has this been spearheaded by anything resembling a development agency. China’s footprint runs through its policy and commercial banks, exports credit agencies and state owned and private firms. and a labour force that has at times exceeded a million workers across Africa. The Gulf’s runs through sovereign wealth funds, firms like DP World and Mubadala, and securing concessions in logistics, oil and gas, and renewables.

These outward investment drives have not been positioned as gestures of altruism, but as mutually beneficial investments. Motivations have included capital surpluses to recycle, excess construction capacity to deploy, critical inputs to secure, exerting greater control over logistics routes, securing early advantage in rapidly growing consumer markets and geoeconomic positioning to advance.

The development consequences of these outward investment drives have emerged more as a by-product than a primary goal. They can be substantial, they can promote growth, they can also be deeply problematic, sometimes both at once. However, the scale of the investment flows arising from these economic strategies dwarfs anything the relevant aid budgets do. The transformative effects on host economies is what give these engagements their weight (for better or worse).

The UK has a very different economic model to China and the Gulf countries. The UK does not have capital surpluses to recycle (in fact it needs to draw in international capital to finance its current account deficit). The British state also has a lighter hand to play when it comes to directing where private capital flows. The City of London may be a world-leading provider of financial services, but part of its attractiveness is the state’s ‘light touch’ when it comes to influencing how that money is used. BII has a useful role to play, but it does not have the balance sheet of a Chinese policy bank or Gulf sovereign wealth fund. This sets certain limits on what a UK ‘donor-to-investor’ pivot can plausibly look like.

A more important point is that even in more state-directed models like China and the Gulf, investment flows are not allocated and programmed in the same way that an aid budget is. Economic interactions still depend on the interests of firms, banks, and non-state actors aligning with what state institutions are encouraging, and on those interests overlapping with the interests of partner on the other side. Economic partnerships are not designed on blank canvases; they follow the contours of how partners’ respective industrial strengths and resources respond to each others’ own needs.

The UK’s economic strengths look very different to these comparators. The UK is one of the world’s largest exporters of services. Key industries that draw other countries into the UK’s orbit include finance, law, accounting, consulting, media, video games, and university education[1]. These service industries depend more on the movement of people, ideas and data than on the flows of goods and bricks and mortar. This does not mean the country has no ‘partnership offer’, but it does not easily lend itself to big eye-catching investment commitments.

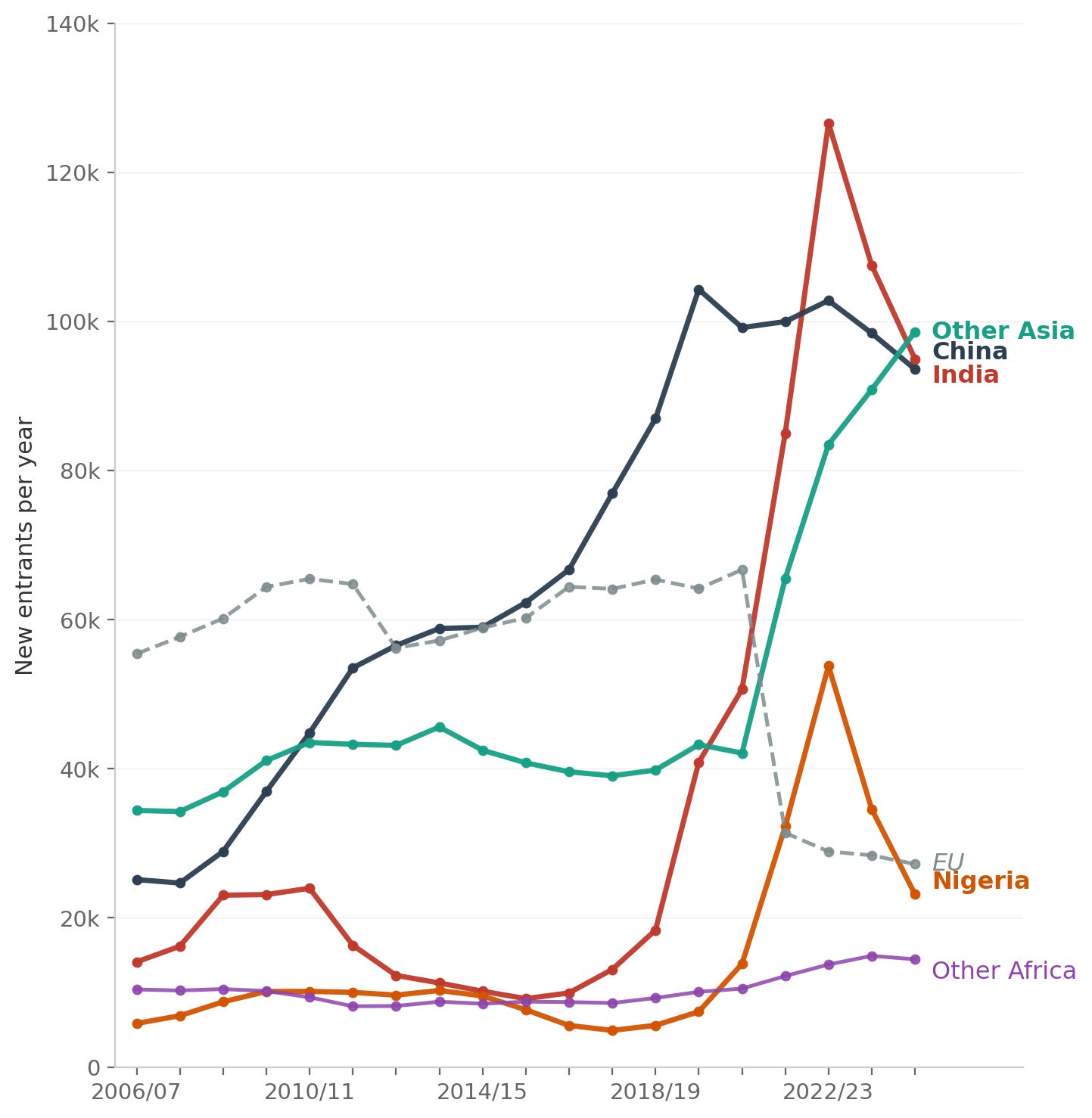

One visible example relates to the UK higher education sector’s increasing reliance on attracting students from emerging markets (especially since Brexit). This includes China, but also historical beneficiaries of UK’s bilateral aid including India, Nigeria, Bangladesh, Pakistan and Nepal. The higher education sector plays a critical role in the UK economy. Innovation in industries including life-sciences, AI and advanced manufacturing can often be traced to research done at UK universities. Universities also support second-city economies (like Manchester, Glasgow, Birmingham, Cardiff, Leeds, Sheffield, and Nottingham) in a country where wealth is overly concentrated in London and the South-East. Attracting international students has become central to the financial sustainability of UK universities. The fees paid by international students underwrite teaching and sustain a research base whose costs domestic fees and funding do not cover.

Trends in international student numbers in the UK

Source: The Higher Education Statistics Authority, ‘Where do Higher Education students come from?’, Chart 6 (January 2026 update)

For prospective students, the offer is the chance to study at a credible institution, but also potentially gain two years of work experience under the graduate route. There is also the possibility of building professional networks and in some cases a longer-term stay in the UK. The English language, a tradition of openness to migrants (relatively speaking) are other selling points.

The time spent studying and working in the UK can potentially provide a formative experience to future political and business leaders. Mo Ibrahim is one such example. He came to the UK for postgraduate work (a PhD at Birmingham in mobile communications) and was then recruited by British Telecom to help design the UK’s first cellular network. He later went on to set up Celtel, which built the first pan-African mobile phone network across 14 countries. (Charles Kenny offers a structurally similar example of Sridhar Vembu in his recent CGD piece on emigration as a growth strategy). The links to development through these kinds of career trajectories are clearly different from those of grant-financed projects providing basic services in low-income settings. They operate on different time horizons, reach different populations, and work through different mechanisms.

The levers for shaping development impact also look different from the ones the donor-to-investor framing implies. They are not primarily about catalysing private capital through institutional vehicles. They are relational and institutional, and they operate in the UK rather than internationally. Regulation can shape who applies, the student experience, and the integrity of the system. The Migration Advisory Committee’s 2024 review pointed to recruitment agents, standards at weaker institutions, and the treatment of dependants as the obvious places to start. Grant makers and foundations could shift from funding international advisers to mentoring individuals as they consider return, supporting work experience, and sustaining collaborations between UK and home-country institutions. The work is closer to shaping the conditions in which talent and ideas circulate than to programming where capital flows. Much of this can be done through universities, individual employers or professional bodies without waiting for a sympathetic government.

Donor to investor - or to something else?

This version of partnership is unlikely to be much discussed next week. The flow of international students to UK universities is not really within the FCDO’s mandate. Flows of money remain the dominant currency of development dialogue even as aid flows are drying up. Anything related to migration is seen as a minefield to avoid. The recent ban on students from Sudan, Afghanistan, Cameron and Myanmar are part of a wider competition over who can adopt the most hostile posture toward migrants. There is a strand of British economic thought, associated with Reform and parts of the Conservative right, that sees the country’s reliance on migrant flows as a symptom of economic weakness to be cured rather than a comparative advantage to be built on. Polling on student migration[2] suggests attitudes may be more permissive than the political conversation suggests, but the political conversation is what drives the window for policy discussions.

Set the political conversation aside for a moment and a picture of a different kind of partnership comes into view. It is not run by the British state. It is not coordinated through bilateral agreements or summit communiqués. It is the cumulative result of universities, research institutes, professional bodies, students, families, and employers making decisions that happen to align. It involves Nigerian families looking for credible degrees, British universities looking for international fee income, researchers looking for collaborators with complementary expertise.

The example of universities matters not just for what it says about the higher education sector, but for what it reveals about how the UK thinks about partnership. The development conversation has been organised around the slice of the relationship that civil servants design and ministers announce. It focuses on the flows of public money to specific countries for specific purposes. That slice is shrinking, and the parts of the relationship that are growing are ones the UK government does not get to programme.

The question then is whether to recognise the partnership that has already emerged, or to keep talking about partnership as if it were about something else that can be moulded to suit more comfortable development narratives. The answer is being given anyway, in lecture halls, research labs, graduate employers and family decisions taken thousands of miles from London. It requires recognising what is real and valued in what the UK has to offer.

[1] See for example this essay by Springford and Sissons or the work of the Resolution Foundation on the structure of the UK economy which describe the UK’s strengths in services industries. Not everybody agrees that this is a good thing. See for example UK Onward’s proposals around Reindustrialising Britain.

[2] Polling consistently shows that public attitudes to international students are markedly more positive than to migration generally. A majority do not want student numbers reduced although this might be linked to how questions are asked. See for example British Future and the recent Comment is Freed post by Sam Freedman