Pushing on a string

How the balance of payments can limit international investment in energy systems

1. The geoeconomic case being made for renewables

The case for investing in clean energy has been quietly rewritten over the past few years. The Middle East conflict is the latest chapter in a line of argument that increasingly justifies investments in renewables as the smart geoeconomic move and not just an investment in protecting the planet.

The Chief of the International Energy Agency has stated:

I expect one of the responses to this crisis will be [an] acceleration of renewables. Not only because they are helping to reduce the emissions but also, they are [a] homegrown domestic energy source.

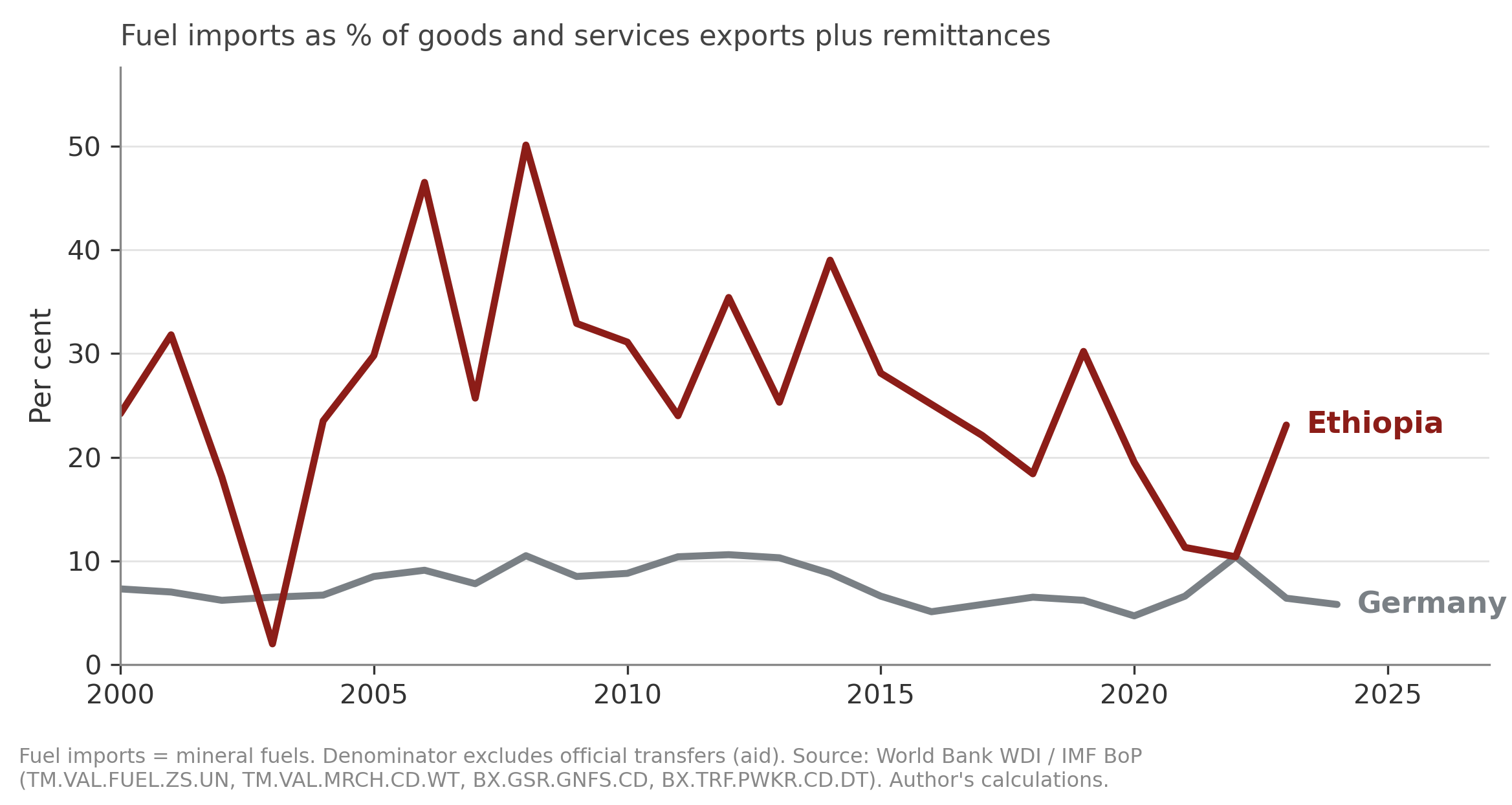

This argument is salient across countries that rely on fossil fuels, but this vulnerability varies in scale. Ethiopia is an example of an economy that is acutely exposed to the volatility of international markets for fossil fuels. The figure below shows the scale of Ethiopia’s fuel imports relative to sources of foreign exchange across the economy, compared to an industrialised fuel-importer like Germany with a diversified industrial base.

Figure 1: Comparing exposure to fossil fuel imports

Given this exposure, it is not surprising that Ethiopia has been looking to make greater use of its abundant hydropower potential. More than 90 percent of Ethiopia’s electricity is generated by domestic renewables, with the Grand Ethiopian Renaissance Dam now operational. In January 2024, Ethiopia became the first country in the world to ban the import of internal combustion engine vehicles. This was not motivated by ardent environmentalism but a deliberate attempt to reduce import bills, having recently defaulted on its sovereign bonds.

The standard argument that I hear at conferences is that the main barriers to building out renewable energy systems are financial: the capital is there, it is just not being invested in the right place. The thesis points to the insufficient scale of finance relative to needs. Plugging that gap requires more private finance because of public budget constraints. Mechanisms need to be found to reduce the cost of capital in lower income countries, especially because of the high up-front capital costs in renewables relative to other energy investments.

This is all good and well, but you rarely get much of a sense of what would actually be needed to sustainably draw in and absorb increased flows of capital beyond a rather superficial discussion about the thin pipeline of bankable transactions. There is a macroeconomic arithmetic that is often overlooked. It bites hardest in lower-income countries that need to expand their energy systems but face binding constraints on foreign exchange.

2. Renewables require imports too

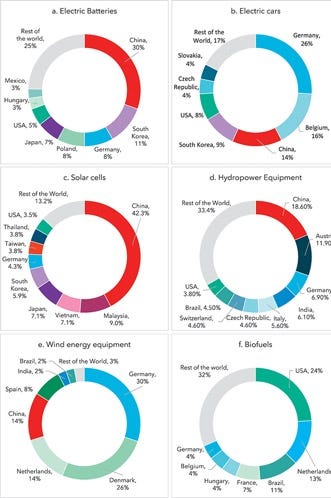

While renewables may be domestic in their ‘fuel’, they are largely imported in their hardware. Solar panels, wind turbines, inverters, transformers, batteries, transmission infrastructure are overwhelmingly produced in a small number of industrialised economies (see chart below). The fuel imports that these technologies displace are not replaced by a costless natural resource; rather they are replaced by capital equipment that itself has to be paid for in foreign currency.

Figure 2: Export market shares of various low-carbon technologies by country in 2020 (retrieved from Survival of the Greenest, Amir Lebdioui, 2024)

Building out an energy system is not a single project, or even a portfolio of projects. It is a sustained programme of installations stretched across years or decades that might include solar parks, wind farms, transmission upgrades, grid storage, distribution modernisation and electric vehicle networks. At the project level, the financing of each asset can potentially be structured to produce a manageable life cycle. At the national level, what the country faces is a sustained surge of capital goods imports, and it has to find the foreign exchange to pay for them. Even where the financing is arranged domestically in local currency, the underlying dollars (or yuan or euros) to settle the equipment still have to be sourced from the country’s overall external position.

In an ideal situation, investment in the energy system stimulates a response in the tradeable goods sector. Firms and farms that could not previously access reliable power become able to compete in international markets, and the export earnings that follow service the claims the build-out created. However, this response is by no means guaranteed.

In its absence, the foreign exchange has to come from somewhere else. The country can borrow to meet its external obligations, but this defers the problem rather than resolving how the imports will ultimately be paid for. It can draw down reserves, but reserves are finite and exist to absorb shocks the country cannot otherwise withstand.

This leaves import compression: essentially the dollars spent on solar panels and transmission infrastructure are dollars not spent on something else that the country imports (e.g. food, medicine, machinery, intermediate inputs for domestic industry). In an energy-rich economy like Germany, the offset can come from the avoided fuel imports themselves. The installation that creates the financing claim also displaces fossil generation that would have required imported fuel, freeing up the foreign exchange to service it. The argument does not hold so well in a country like Ethiopia, where firms and households would consume far more energy if incomes allowed. Substitution alone does not generate the foreign exchange to service the claim; growth in tradeable production (or remittances) has to do that work.

3. When the FX constraint bites

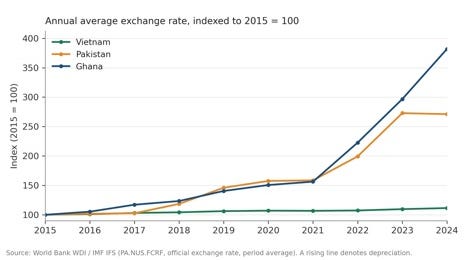

This is not just a theoretical concern: Pakistan and Ghana illustrate the dynamic (even if the technologies in question were largely thermal rather than renewable). Both countries have undertaken substantial power expansion programmes financed through dollar-indexed contracts: Pakistan through successive waves of contracts for independent power producers since the mid-1990s; Ghana through the post ‘dumsor’ procurement push of 2014–2017 that produced 43 power purchasing agreements.

At the project level the contracts were successful in attracting private investment (the projects were ‘bankable’. Plants were built and generation capacity was added, but the overall push to increase power generation has given rise to major financial difficulties. There was PKR 2.6 trillion of ‘circular debt’ in Pakistan by 2025; the government of Ghana cleared $1.47 billion of legacy energy sector debt earlier this year. Roughly thirty to thirty-five percent of Pakistan’s consumer electricity tariff now consists of debt servicing rather than energy costs.

There have been a series of reports (see examples here for Pakistan and for Ghana) documenting some of the shortcomings in approaches to procurement and utility management. Proposals to improve procurement, take alternative approaches to contracting, and improve cost recovery are all valid.

There is also a macro challenge here that compounds these difficulties within the power sector. Capital flowed into the power sector at scale, on terms that made individual projects bankable for international sponsors. The resulting obligations were denominated in foreign currency, but the country’s capacity to generate that foreign currency has not kept pace with the cumulative obligations being created. Macroeconomic adjustment forced the country to compress not only demand for power, but also for imports across the economy as exchange rates devalued.

A contrast with Vietnam is instructive here. Vietnam also expanded power generation rapidly over the past decade and much of it under a feed-in tariff regime that drew in international capital. Like Pakistan’s and Ghana’s arrangements, contracts were denominated in or indexed to hard currency. Vietnam’s power sector has not been trouble-free: there have been disputes over curtailment and delayed payments to renewable developers, and the state utility’s finances have come under strain. But that stress stayed contained within the sector. It did not escalate into a balance-of-payments crisis, because the dong remained broadly stable: manufacturing-led export growth continued to generate the foreign exchange to service the obligations as they accumulated. The contracts created similar foreign-currency claims; what differed was the capacity of the wider economy to absorb them.

Figure 3: Comparing exchange rate movements against the US dollar over the past decade

Balance of payments constraints need not show up as a Ghana-style stress event. The more common pattern is one where insufficient capital is flowing because of a perceived lack of ‘bankable projects’. Project bankability is not just a function of project preparation and the capabilities to undertake good feasibility studies. It is also a function of the country’s external position. Innovations like local currency lending can shift who bears that risk, but they cannot eliminate it; the risk shows up in the cost of the project somewhere. Work to improve project finance structures may do useful work at the margin, but the cost of capital is at least partially endogenous to the country’s external account. The architecture’s emphasis on instrument innovation at the project level cannot transcend a constraint that operates at country level.

4. How to absorb more capital

None of the above should be read as an argument against upscaling investment in clean energy systems, rather it is a suggested corrective on where energies should be focused. ‘Unlocking’ climate finance is not just an up-front financing problem; a sustained increase in capital imports also requires sustained growth in ongoing foreign exchange earnings. Expanding the availability of foreign exchange is a precondition for absorbing the capital flows that the international financial architecture is ostensibly trying to mobilise.

There is of course a horrible chicken-and-egg problem here. Firms in low-income countries consistently identify unreliable electricity as a binding constraint on their growth and particularly growth in tradable goods and services whether that be garment factories in Ethiopia, agro-processing in Tanzania, or digital services in Nigeria. All face power costs and reliability problems that limit their competitiveness in international markets. Building out power requires sustained inflows of foreign exchange, which requires exports: a country needs power to grow exports, and exports to fund power.

The link between power investment and tradeable production deserves more weight than it typically receives. Direct electricity exports are one way to make the arithmetic work. Ethiopia is pursuing this approach, anticipating exports of hydro-generated electricity to neighbouring countries, but when it comes to renewables, this model depends a lot on the demand and infrastructure of your neighbours. For most countries the indirect route matters more: power investment that supports export diversification through industrial development, processing of agricultural and mineral exports, or services exports that depend on connectivity.

At the national level, the structures oriented to tackling constraints to exports are not the same as those required for coordinating flows of money. Less focus would be paid to coordinating different donors (through e.g. country platforms); more would go to the coordination mechanisms between government and the productive economy itself, particularly the firms that would generate an export response. Less time would be spent coming up with ever more elaborate efforts to link fiscal systems to climate concerns; and more about surfacing and addressing concrete operational constraints faced by firms such as customs delays, input availability, skills gaps or regulatory barriers.

None of this may be a revolutionary insight, but it does feel like greater scepticism is warranted about the idea that the world’s largest asset managers hold the secret to unleashing a wave of clean energy investment. For many lower-income countries the constraint is not the capital on offer but the capacity of the economy to absorb it: to earn the foreign exchange that the imported hardware, and the obligations attached to it, will eventually have to be paid in. The harder question, and the more useful one, is what it would take to absorb more capital. Otherwise efforts to engineer ever more elaborate financing structures and strategies will feel like pushing on a string.

This is a great post. I had sort of circled around this point in my mind but without appreciating it as a key constraint. It feels very relevant to some of the Mission 300 discussion on connecting households v connecting companies: I imagine the export elasticity of connecting firms to the grid is much higher than to putting solar panels on roofs in rural areas…

It isn't just renewables though surely, but any situation where large, prolonged investments are needed and are dependent on imports, but have (at best) an indirect and distant impact on forex? (I had been thinking about something similar in the case of natural disasters, which could have a big hit on productive capital that then needs to be replaced, probably with imports. But obviously that would just get export capacity back to where it was rather than increasing it, so there must be a forex hit)

Does it also make you think differently about some ‘mutual benefit’ investments from Europe/China, with explicit focus securing access to commodities? I suppose these could plausibly generate their own export revenue directly. E.g. I’m extremely sceptical about some of the green hydrogen stuff the EU is doing given the economics of it. But if, say, you invest in a ton of solar capacity in Namibia and can use excess generation at non-peak times to power electrolysers to make ammonia, perhaps the BOP dimension makes it slightly more favourable..

Do fossil fuel - exporting countries that subsidize domestic oil, gas, and coal consumption have a nice feedback loop awaiting them where they can sell fossils to buy EVs, PVs, wind, batteries etc, replace subsidized fuels and export the fuels they would have burned domestically to pay off loans for cleantech capital costs? Should we expect South Africa, Libya, Nigeria to be cleantech leaders?

Will GLP1s lower junk food imports a lot? Will they make fuels made from corn and sugar cheaper?