Hostage to fortune?

On trade shocks, the limits of fiscal adjustment, and the slow hard work of building economic resilience

1. The external conjuncture

Speaking to the Mirror before flying to Washington for this year’s IMF Spring Meetings, UK Chancellor Rachel Reeves made no attempt to hide her frustration. “I feel very frustrated and angry that the US went into this war without a clear exit plan, without a clear idea of what they were trying to achieve,” she said of the US-Israeli military action against Iran. This was, she emphasised, “a war that we did not start” and “did not want.” The Resolution Foundation estimated that the average British household stood to be £480 worse off over the year as a direct result of the conflict, not because of anything the UK government had done, but because of decisions made in Washington and Tel Aviv.

For African finance ministers arriving at the same Spring Meetings, the experience of having your economy knocked sideways by decisions made elsewhere is not a shock. It is a permanent fixture of the job.

As Thandika Mkandawire once observed1:

“Most analysts underestimate the enormous importance to African economies of external conjuncture… African economies generally do well when the global conjuncture is good and poorly when it is bad. This is a lesson that the Bretton Woods Institutions have gradually learnt as their own stabilisation and adjustment programmes have on several occasions been unscrambled by external factors.”

This recognition sits awkwardly alongside the dominant language of economic policy advice directed at Africa. There remains a persistent presumption that if finance ministries could simply get the public purse in order - raise more taxes, spend within their means, improve debt management — then growth and resilience would follow. The IMF’s most recent annual report2 on Macroeconomic Developments and Prospects in Low-Income Countries, (which covers much of sub-Saharan Africa) illustrates the point:

“Building resilience and reinvigorating growth remain urgent. This agenda calls for continued fiscal consolidation in most LICs, with pace and calibration tailored to country circumstances, and supported by stronger domestic revenue mobilisation, expenditure prioritisation, and improvements in public financial and debt management.”

This is not necessarily wrong advice as far as it goes. In a crisis, governments often have no choice but to tighten their belts. But it starts from the wrong place. The question worth asking is not how to manage the pain of an external shock once it arrives, but why some economies are structurally more exposed to those shocks than others — and what determines their capacity to absorb them without resorting to painful adjustment. That is often more a question about the balance of payments than the budget.

2. When external developments dominate economic management

In a 2011 article, José Antonio Ocampo challenged the idea that “fiscal dominance” (excessive government borrowing crowding out private investment and stoking inflation) is the primary driver of macroeconomic instability in lower income countries. He argued that in lower-income contexts, short-term macroeconomic dynamics tend to be predominantly shaped by external shocks, positive or negative. He calls this “balance of payments dominance”.

Two channels matter most. The first is the boom-bust cycle of international capital flows. External finance becomes readily available during boom periods and then abruptly dries up or becomes prohibitively expensive during crises. Where demand for foreign currency outstrips supply, exchange rates come under pressure. Currency depreciation raises the domestic cost of servicing dollar-denominated debt, tightening fiscal space precisely when it is most needed. Depreciation also raises the cost of imported goods (which might include certain food-stuffs and fuel), it feeds directly into inflation, and complicates monetary policy.

Since the Covid-19 pandemic, these dynamics have been acute – and well documented. For example, Boston’s Global Development Policy Center has tracked the retreat of Chinese lending to Africa. The Finance for Development Lab has documented how access to international capital markets tightened and costs rose. Eurobond spreads for many African issuers reached levels that made new borrowing effectively impossible. Aid cuts have also denied countries precious resources often earmarked for the provision of basic services.

The second channel is trade. Many African countries are currently facing significantly larger import bills as a result of the Middle East conflict. But vulnerability to trade shocks is a perennial challenge for economies that rely on a narrow set of primary commodities to generate their export earnings. When commodity prices fall or import costs rise, the external constraint tightens regardless of how well the fiscal house is managed.

3. Reading foreign exchange constraints – the case of Tanzania

To make this concrete, consider what Tanzania’s balance of payments actually looks like over time.

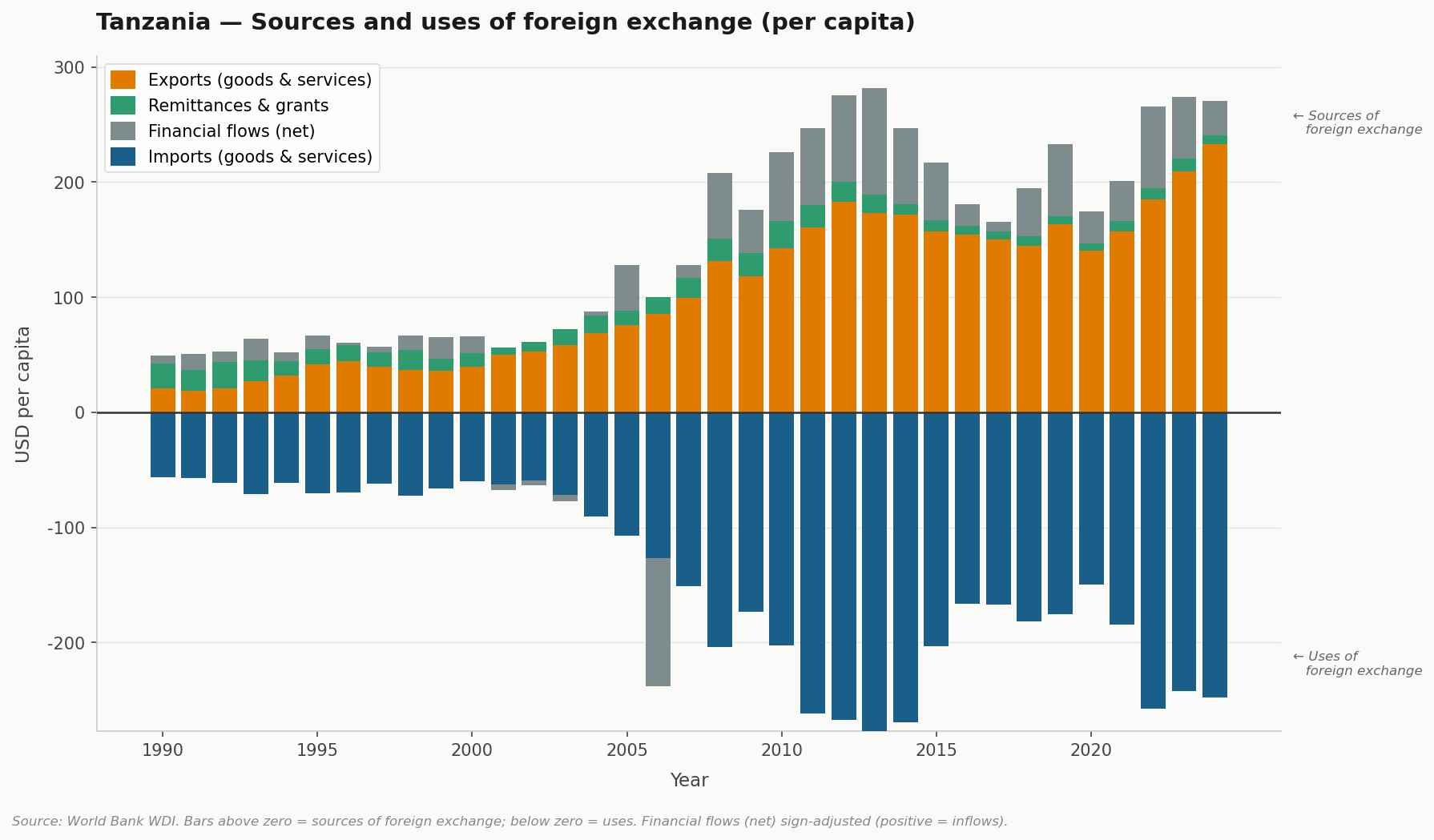

Chart 1: Tanzania balance of payments in USD per capita, 1990–2024. Blue bars below the line show imports. Orange bars show export revenues. Green bars show grants and remittances. Grey bars show net financial flows including external borrowing.

Several things stand out. The first thing to note is the scale of the constraint. Around the year 2000, Tanzania’s export earnings were equivalent to approximately $40 per capita. When aid, remittances, and concessional borrowing are added in, the country had sufficient foreign exchange for imports worth roughly $60 per person. That is $60 to cover all the things that are not produced in Tanzania. It is barely enough to cover basic consumption, let alone the import-intensive investment that sustained structural change requires.

A second key observation relates to how that constraint has shifted across different periods. In the 1990s, export earnings were stagnant. They began to grow in the 2000s, partly on the back of the global commodity super-cycle. In the 2010s, export growth tailed off, but import growth was sustained through increased borrowing (the grey bars expanding to fill the gap). The early 2020s brought a sharp contraction in net financial flows, but export earnings have since begun to recover.

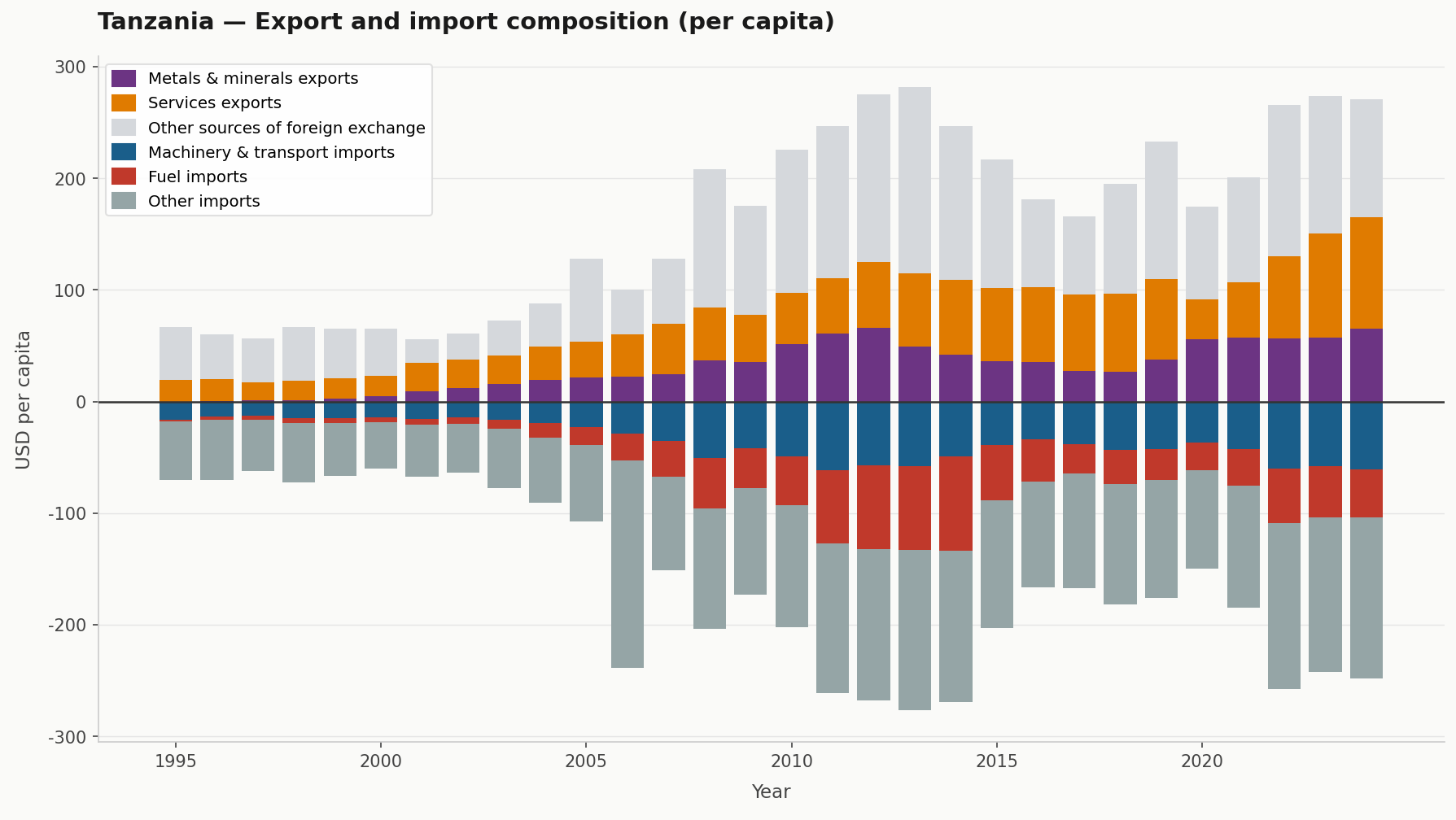

Different factors are at work in driving export growth. Tanzania, like other African gold exporters, has benefited from sharp rises in gold prices, driven in large part by gold’s rising appeal as a ‘safe-haven’ asset (and likely a good dose of speculative fervour in international financial markets). Tanzanian coffee exports have grown (along with Ethiopia and Uganda) partly because climate shocks in Vietnam and Brazil, the world’s two largest coffee producers, have disrupted global supply. These gains are in a sense ‘windfalls’ driven predominantly by the ‘global conjuncture’ that may not be sustained.

The growth in services exports tells a different story. Services exports, driven by tourism revenues have roughly doubled on a per capita basis over the past fifteen years. Unlike gold, this is not primarily a function of global prices: it reflects a decade of deliberate investment in infrastructure, access, and positioning.

Chart 2: Export and import composition in Tanzania in per capita USD, 1990 - 2024

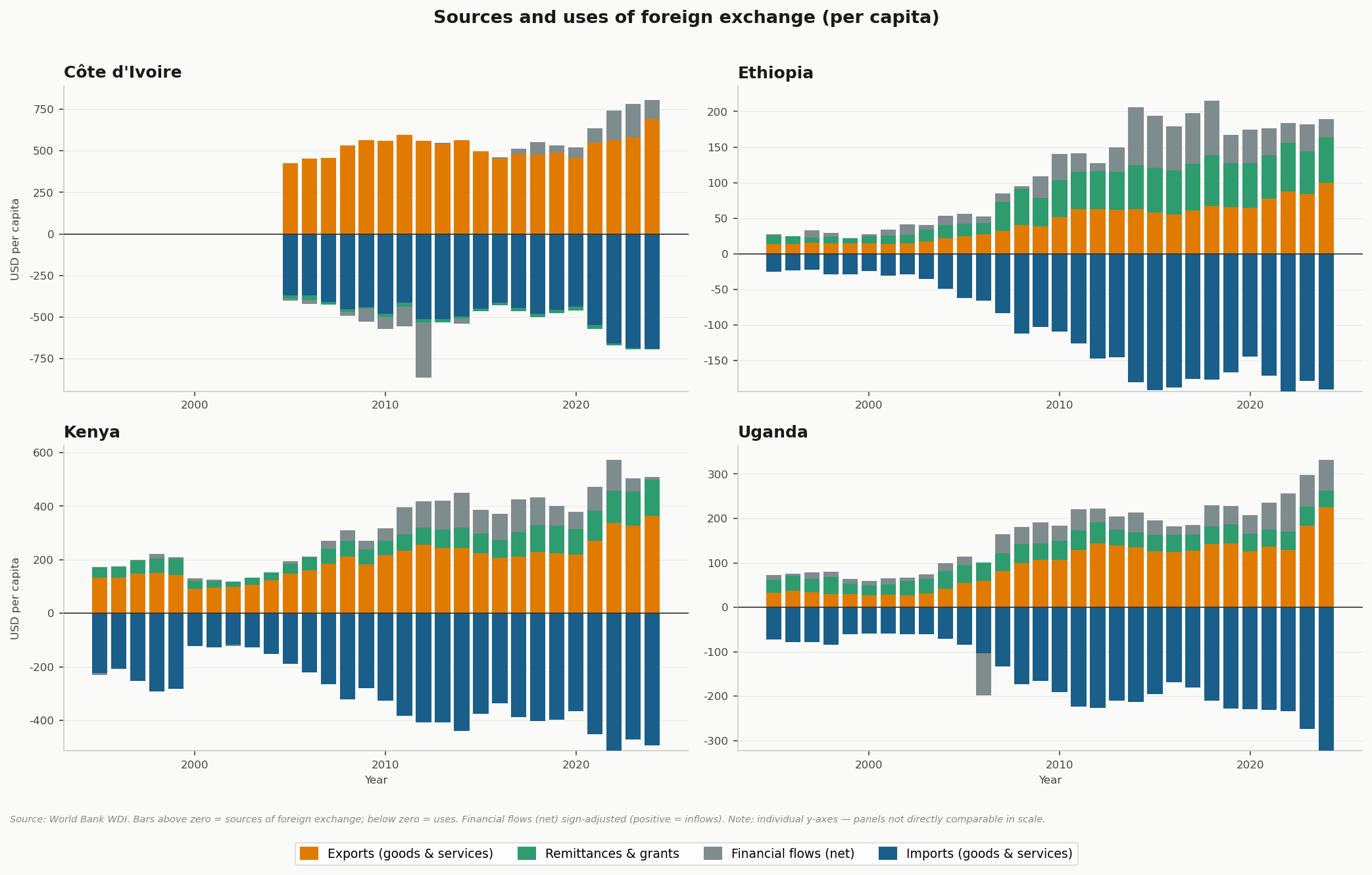

Tanzania is not a lone example. Similar patterns of export growth are visible across other major sub-Saharan African economies. The panel below shows a recovery of export earnings in the 2020s across a range of non-fossil-fuel exporters. In each case, improved export earnings have helped counterbalance some of the pressure arising from tighter international monetary conditions.

Chart 3: Export earnings recovery in selected sub-Saharan African economies

The pattern matters because of what happens at the extremes. When foreign exchange constraints bite— as they did for many African economies in the early part of this decade — currencies come under pressure, the local cost of dollar-denominated debt rises, imports become more expensive, and governments face pressure to cut spending precisely when households are most stretched. The boom-bust dynamic is one reason that growth in Africa has tended to be episodic.

When export earnings rise, the same mechanisms work in reverse: the currency stabilises, debt service costs ease in local terms, and governments retain room to maintain spending without receiving a single dollar of export revenue directly.

The magnitudes involved can dwarf official finance flows that are pored over by analysts. Data from the Bank of Ghana shows that Ghana’s formal gold exports surged to over $20 billion in 2025 — almost double the previous year — driven partly by rising prices and partly by the formalisation of artisanal mining through the new Ghana Gold Board. The IMF’s entire three-year balance of payments support programme came to $3 billion. IMF support provides genuine credibility and policy anchoring that the numbers alone do not capture. But the relative scale is striking: the most powerful determinant of whether Ghana needed to impose painful austerity was not the quality of its fiscal management. It was the price of gold.

4. Beyond the fiscal consolidation fix

None of this is a counsel of fatalism. Recognising the primacy of the external constraint does not mean that domestic policy choices are irrelevant, or that governments should simply wait for commodity prices to turn in their favour. It does mean redirecting attention toward the structural drivers of macroeconomic stability.

Fiscal consolidation manages the symptoms of external vulnerability. It does not reduce the vulnerability itself. That requires something harder and slower: growing the volume and diversifying the composition of export earnings, so that structural change becomes financeable and external shocks become absorbable.

Tanzania remains highly exposed to events in the Middle East because of its geography and the structure of its economy. But fuel imports that absorbed half of export earnings a decade ago now absorb perhaps thirty to thirty-five percent — not only because the export base diversified, but because it grew. Back in 2000, Tanzania had just $40 of export earnings per person to finance everything the economy could not produce domestically. That number has risen substantially. The constraint has not disappeared, but it has loosened a little, and that loosening is what resilience actually looks like in practice: not the ability to avoid shocks, but a reduced susceptibility to being overwhelmed by them.

The external conjuncture will keep changing. Commodity prices will rise and fall. Conflicts will break out in places that move energy markets in ways no finance minister can anticipate.

What governments (and the organisations that advise them) can do is keep a clear view of where the structural vulnerabilities lie, and invest patiently in reducing them.

I first came across this piece when reading Grieve Chelwa’s analysis of Zambia’s debt crisis.

The report was published on March 31st, but seemingly drafted before the invasion of Iran.